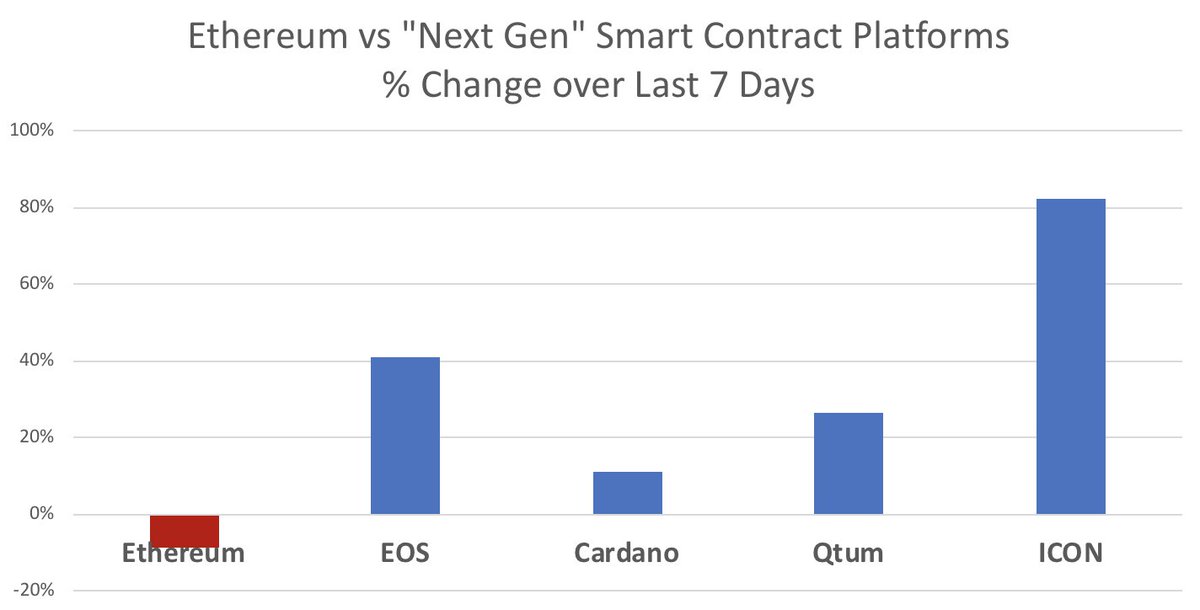

1/ #Ethereum is noticeably soft while many of its "next gen" competitors are showing strong bounces after brutal falls. coinmarketcap.com/all/views/all/

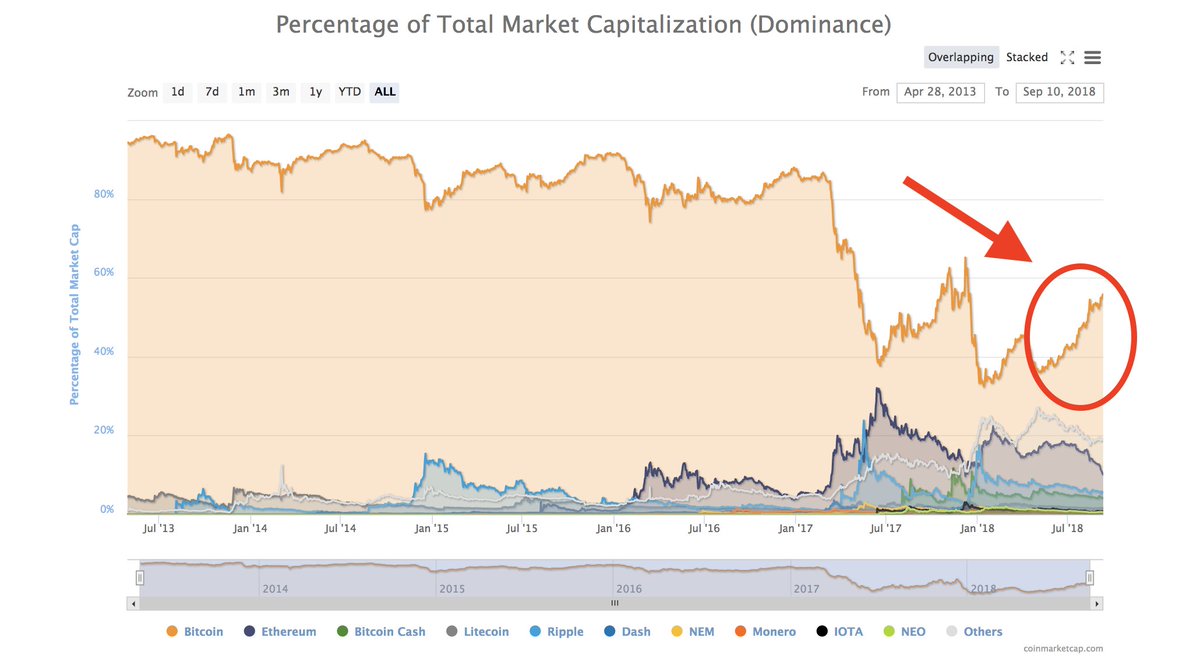

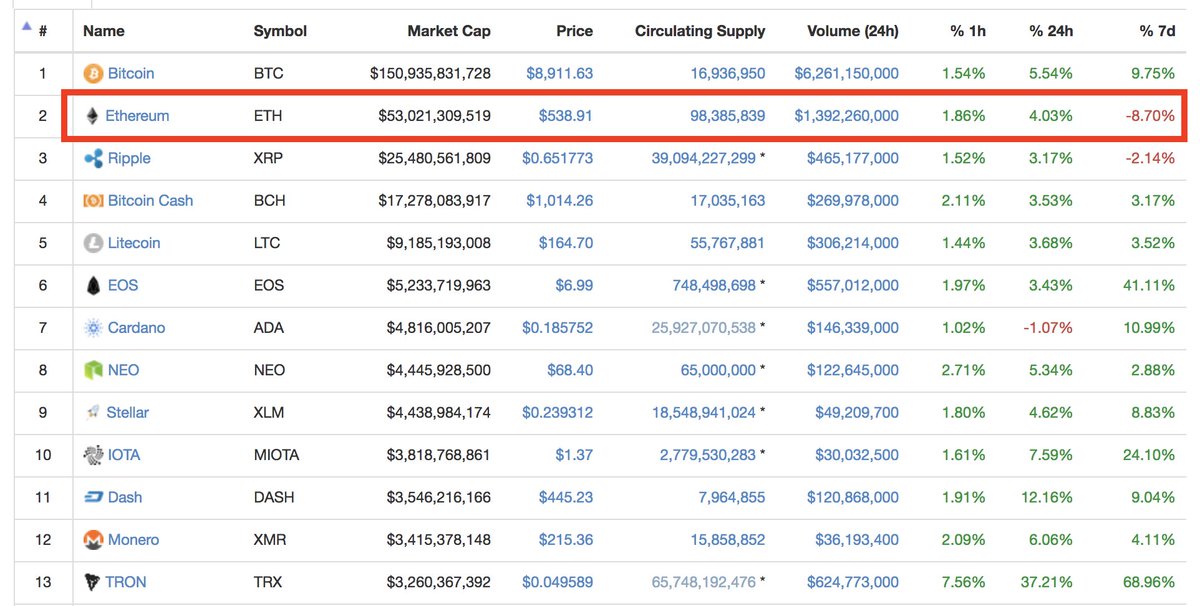

2/ #Ethereum's softness also clear in the context of the top 10. In stark contrast to how this bear market started, where $ETH was one of the most resilient assets.

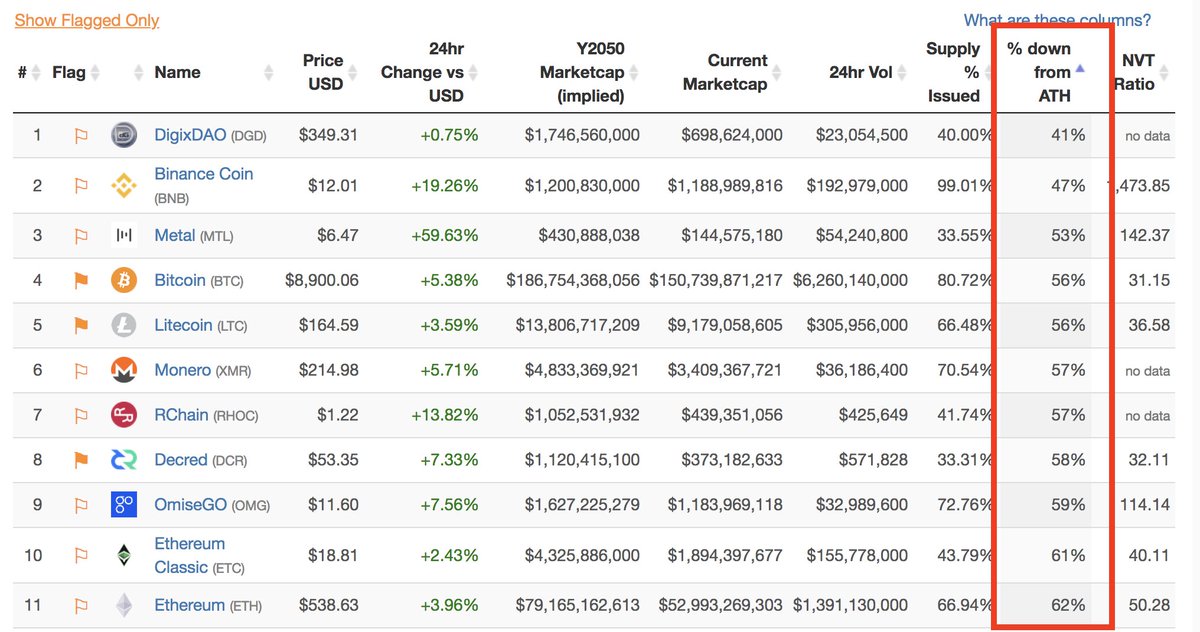

3/ To be fair, #Ethereum is still down less from its all-time high than its aforementioned "next gen" competitors.

4/ But my point is more around *recent* sentiment and how much people are scared by SEC enforcement action, and how that affects $ETH + if people really think $EOS & friends represent a serious threat to #Ethereum's network effect. @dfinity's raise is raising eyebrows...

5/ I still have a hard time thinking it wise to bet against #Ethereum's "feature gravity" & soft network effects, especially given the team's flexibility & speed, but am alert nonetheless.

6/ There has been much-increased talk amongst #dapps of "cross-chain support," which could weaken #Ethereum's value prop along with all other base-layer smart contract platforms, perhaps pushing more value into "middleware protocols."

7/ As with everything else, follow the talent 🙂

• • •

Missing some Tweet in this thread? You can try to

force a refresh