⚠️⚠️ THREAD: Trump/GOP #ACASabotage is costing #ACA enrollees even more than you thought. Here’s why (warning: graphs ahead!)

1/ Every year during the off season, I spend countless hours digging into hundreds of wonky insurance carrier rate filing forms to analyze the weighted average rate increases for the following year.

2/ I then compile a table which breaks these averages out on a state-by-state basis, and I have a pretty damned good track record of accuracy, if I say so myself.

3/ For instance, in 2015, I projected an average unsubsidized rate increase of roughly 12.5% nationally. This was later confirmed to be around 11.6% by @RWJF: acasignups.net/15/12/16/well-…

4/ In 2016, I projected an average rate increase for 2017 of about double that...nearly 25% nationally. When the official ASPE report from HHS came out, they pegged it at 22%...but when corrected for non-Silver plans it was a bit higher: acasignups.net/16/10/25/did-i…

5/ Then, last fall, I upped my game: Instead of just looking at the total avg rate increases, I also attempted to break out the PORTION of those increases caused SPECIFICALLY by sabotage efforts by Trump/Congressional Republicans.

6/ In 2017, there were a BUNCH of different things Trump tried to do to kill, hurt, weaken, undermine or otherwise damage the #ACA. Some were successful. Some partly worked. Some utterly failed. It was a chaotic maelstrom of deliberate dickishness on his part.

7/ Trump slashed HealthCare.Gov 's marketing budget 90%. He slashed the outreach/navigator budget 40%. He slashed the Open Enrollment Period in half. He told the IRS not to enforce the mandate (they confused EVERYONE by first saying they wouldn't...then that they would).

8/ Meanwhile, Congressional Republicans spent the first half of the year desperately trying to repeal the #ACA (and kind of, sort of "replace" it) with one Godawful pile of crap after another.

9/ This caused further confusion. Millions had no idea if the law was about to be repealed, or already had been. Some were desperate to enroll figuring it was their last chance...others deliberately avoided doing so thinking that they'd have the rug yanked out if they did.

10/ Then, in mid-October, Trump unleashed what he THOUGHT would be his nuclear bomb: He cut off Cost Sharing Reduction reimbursement payments. He THOUGHT that this would instantly destroy the entire #ACA exchange system, causing it to "explode" in his own words.

11/ However, the state insurance commissioners put their heads together with the state-based #ACA exchanges and the insurance carriers themselves and came up with a clever workaround called #SilverLoading. This didn't completely counter Trump's sabotage, but it mitigated it.

12/ Instead of dropping out of the #ACA market altogether, most of the carriers ended up "loading" that CSR cost onto their Silver policies only. Subsidized enrollees were protected from rate hikes, but *unsubsidized* enrollees in many states took the hit with large hikes.

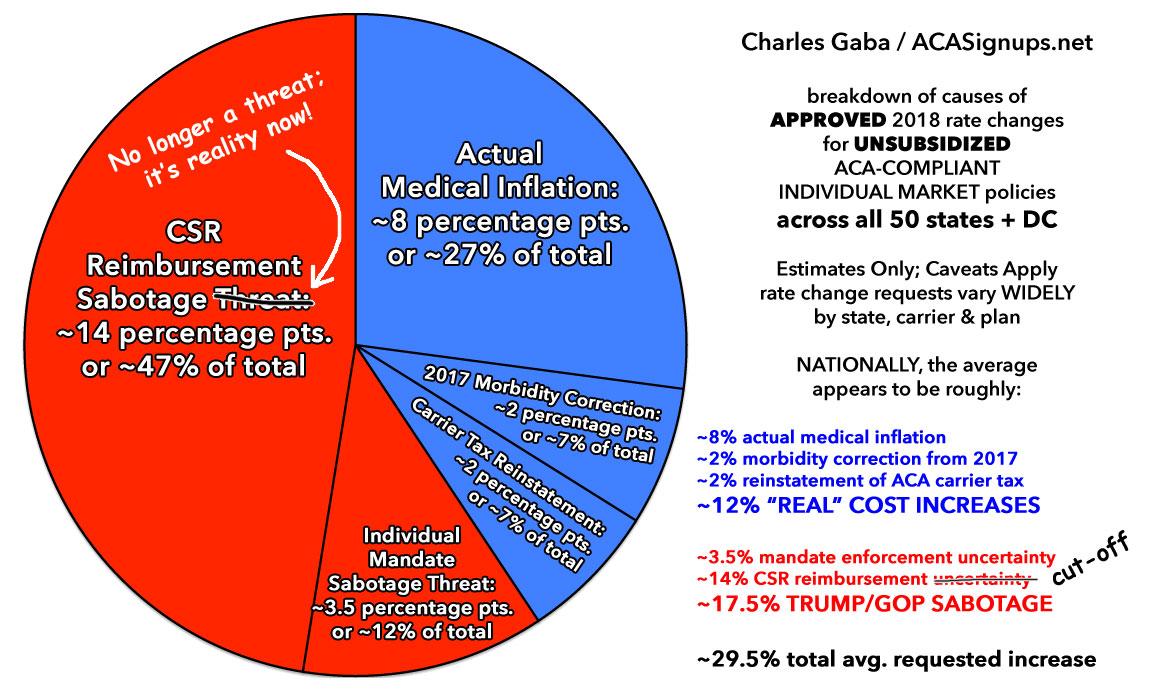

13/ Many of the carriers actually came right out and stated exactly how much of their increases were due to the CSR load. The @KaiserFamFound ran an analysis of the projected CSR load as well, and I used educated guesstimates to fill in the blanks.

14/ In the end I pegged the avg. rate increase at ~29% nationally, with roughly 14 points due to the CSR cut-off, another 3 points or so due to other factors (slashed budgets, half-length enrollment period, general confusion, etc). (no GIF for this one): acasignups.net/17/11/01/and-i…

15/ Well, as it happens, the ACTUAL average unsubsidized 2018 rate increase for individual #ACA compliant policies turned out to be right around...29% nationally: acasignups.net/18/04/09/updat…

16/ So here's the thing: That ~17% #ACASabotage-specific chunk of the 2018 translates into roughly $80/month, or ***$960 MORE*** for the year PER UNSUBSIDIZED ENROLLEE. Obviously this varies widely by state, carrier, and individual policy: acasignups.net/18/04/11/updat…

17/ Now, that was 2017 #ACASabotage, which caused unsubsidized 2018 premiums to spike massively, right? Now let's talk about 2018's sabotage and the expected impact on *2019* premiums.

18/ For 2019, Trump and the GOP are throwing three major NEW types of #ACASabotage at us: 1. Congressional Republicans repealed the #ACA's Individual Mandate Penalty (actually done last December but doesn't go into effect until 2019)...

19/ ...and 2. & 3. Trump issued an executive order stripping away regulations/restrictions on NON-#ACA compliant "short-term" and "association" plans (#ShortAssPlans). Not all of these are actually #JunkPlans but many are, and they don't generally include key ACA protections.

20/ So, how much more will THESE #ACASabotage efforts cause rates to increase? Well, the CBO projected around 10% overall for #MandateRepeal, while other studies indicate anywhere from 2-5% for #ShortAssPlans. Why? Because all of these cause healthy people to drop out...

21/ ...which in turn means that those who stay in the #ACA policies tend to be folks who are sicker, which means they're more expensive to treat, which means higher claims, which means higher premiums, which means more healthy people drop out...

22/ The most comprehensive effort to project this comes from the folks over at the @UrbanInstitute, who gave estimates of the impact of both #MandateRepeal and #ShortAssPlans (well, the "short" part anyway) in each state: acasignups.net/18/06/05/my-of…

23/ They came up with estimates ranging from as little as 0% in Massachusetts (which still has their mandate penalty from Romneycare days) to as high as 21%, averaging around 16.6% nationally. Ouch.

24/ But that was before any of the states started releasing their actual 2019 rate filings. So far about half the states have done so, including the biggest ones (CA, FL, NY, PA and most of TX...still a few carriers missing there).

25/ The GOOD news? Many carriers overshot last fall--the #ACASabotage was real, just not quite as bad as they thought. The #ACA itself LIMITS THEM TO A 20% GROSS MARGIN (the 80/20 MLR rule), so their 2019 increases are lower than expected...or in some case DROPPING a few points.

26/ The BAD news? That #MandateRepeal & #ShortAssPlans sabotage impact is still there. A carrier that would otherwise keep rates flat might be raising it 10%. If they were planning on dropping rates 5% they might be asking for a 6% hike. Maybe a 2 point drop instead of 12.

27/ In Minnesota, for instance, avg. premiums are actually set to DROP about 8% thanks to their "reinsurance" program (explainer here: acasignups.net/18/07/12/my-ha… ). HOWEVER, they WOULD likely drop by more like 15% or so w/out #ACASabotage. acasignups.net/18/06/15/minne…

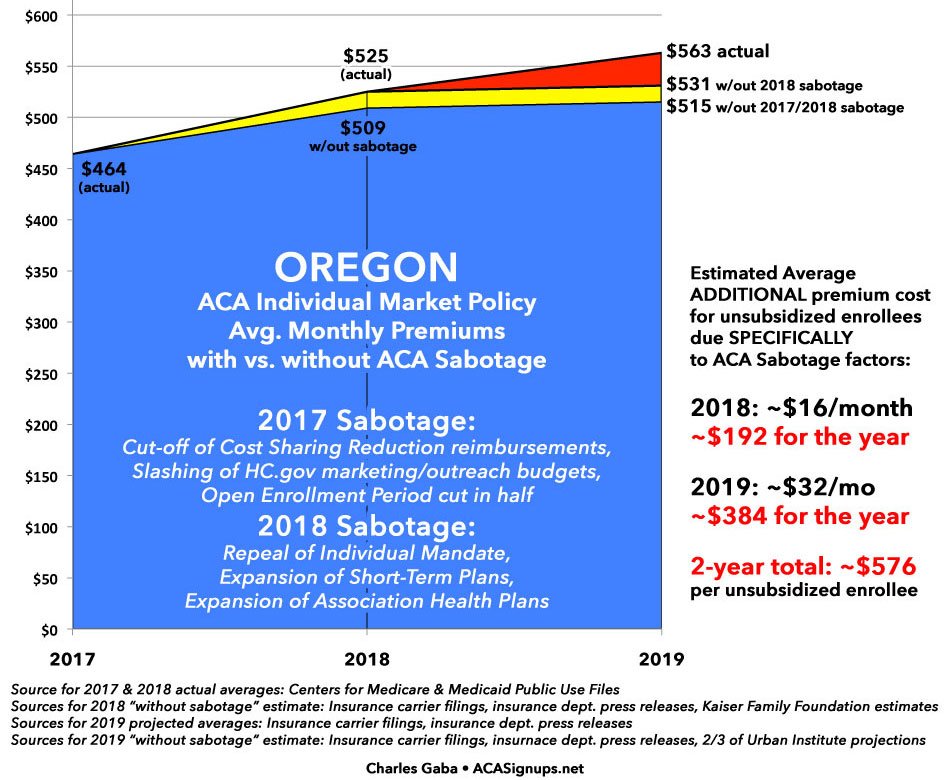

28/ A more typical example is Oregon, where rates *are* going up by around 7.3%, but *would* have only increased by roughly 1.2%. That may not sound like a big difference, but that's around $32/month or $384 for the year: acasignups.net/18/07/21/orego…

29/ So far, across 26 states, I estimate that unsubsidized #ACA premiums are going up around $625 per enrollee for the year due SPECIFICALLY to the latest round of sabotage efforts: acasignups.net/18/07/23/updat…

30/ FINALLY, I GET TO THE POINT OF THIS THREAD: When measuring the financial "sabotage tax" unsubsidized enrollees pay, you have to include BOTH years...and remember that even if the rates *drop* next year, you'll still be paying more than you would *without* #ACASabotage.

31/ Here's two examples: First, Oregon, where the impact has been *relatively* mild both years: Around $192 this year plus another $384 next, for a total of around $576 per enrollee. That's around $2,000 for a family of 4. acasignups.net/18/07/25/how-m…

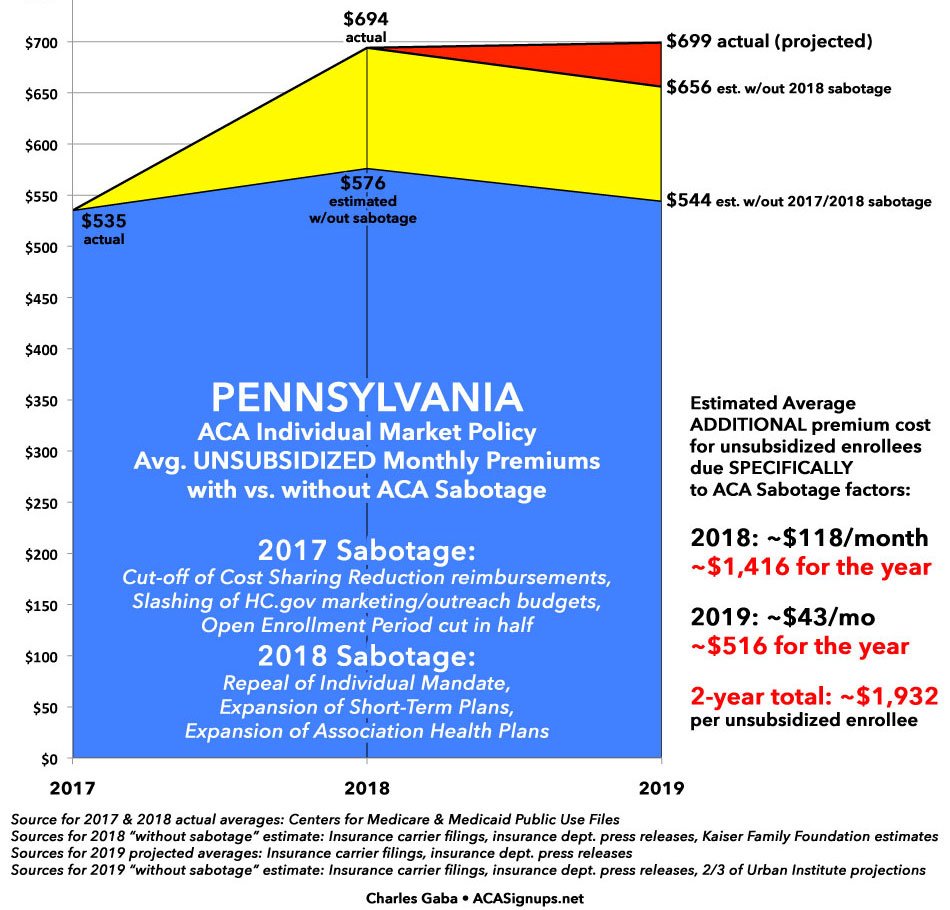

32/ ...and Pennsylvania. No, that's not a typo: As far as I can tell, an avg. of $118/month of this year's *unsubsidized* increase is due to #ACASabotage, plus another $43/month for next year (even though the actual rates are only going up slightly): acasignups.net/18/07/25/how-m…

33/ I'll be adding more states over the next few weeks at this link. The bottom line is that Paul Ryan's $1.50/week CostCo tax cut is being more than cancelled out by his/Trump's #ACASabotage for millions of people. acasignups.net/18/07/25/how-m…

34/ And with that, I'm going to bed. If you'd like to support my work and are in a position to do so, please feel free to help out here, thank you!

https://twitter.com/charles_gaba/status/954188046676742150

• • •

Missing some Tweet in this thread? You can try to

force a refresh